Ecommerce Accounting Explained: Cost of Goods Sold (COGS)

Want to feel totally confident in your bookkeeping? Our Essential Ecommerce Bookkeeping Checklist is your roadmap to bookkeeping success. Download it for free to enjoy tidy, reliable accounts from now on.

“If you want to make business decisions you need to understand your KPIs. Your margin is the most important one. It allows you to understand whether your products are making money.”

- Lior Zehtser, Co-founder, ConnectCPA.

Margins help you figure out whether your business is profitable.

But you can’t work out your margins without understanding Cost of Goods Sold (COGS).

A2X spoke to Lior Zehtser from ConnectCPA about all things COGS. Together we’ll explain what COGS is, how to calculate it, and how to use it to increase profitability.

In this guide to COGS, you’ll learn:

Table of Contents

Want to feel completely confident in your ecommerce bookkeeping?

Businesses that document their processes grow faster and make more profit. Download our free checklist to get all of the essential ecommerce bookkeeping processes you need every week, month, quarter, and year.

Download it here

What is COGS?

“Cost of goods sold are the expenses incurred for a product you’ve sold.”

- Lior Zehtser, Co-founder, ConnectCPA.

COGS, also known as “cost of sales”, is the direct cost of producing the inventory your business has sold.

Direct costs are everything you pay for to get your inventory ready for sale.

Inventory is anything you take possession of to sell to customers.

You can calculate COGS with this formula:

COGS fluctuates depending on the price of your inventory and how much you buy or sell. So you’ll need to keep track of it consistently.

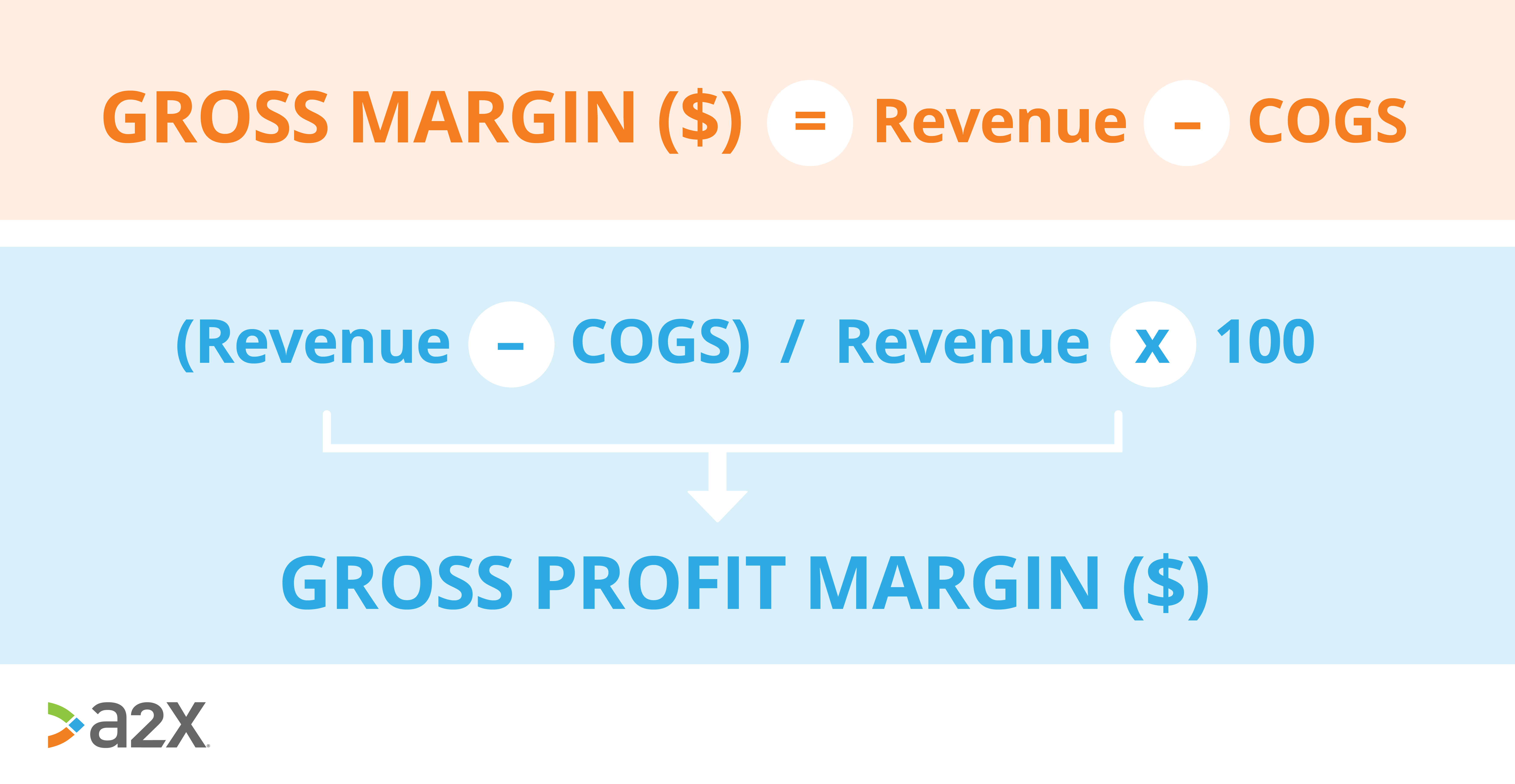

Why is it important to keep a clear understanding of your COGS?

COGS gives you visibility over the health of your business.

Most notably, COGS lets you calculate your

gross profit and gross profit margin.

If these figures are too low you won’t have enough money for operating expenses. Your business won’t make a profit.

You can improve your margins by increasing your prices or lowering your COGS.

What’s included in Cost of Goods Sold?

“A good litmus test to determine whether something should be included in COGS is to ask: Would the cost exist if no products were produced? If the answer is no, then the cost is likely included in COGS.”

- Scott Beaver, Sr. Product Marketing Manager, NetSuite.

COGS includes only the direct costs of acquiring or creating your products.

Figuring out what counts as a direct cost can be tricky, especially for ecommerce sellers.

You might be acquiring a product, manufacturing a product, or a mixture of both. And you might be using a third-party logistics (3PL) company to store and distribute your products.

Let’s take a closer look at what’s included in COGS for ecommerce sellers.

“COGS includes everything it takes to get your inventory from your supplier all the way to your warehouse and ready to sell to your customers.”

Here’s what’s commonly included in COGS:

-

The cost of purchasing a product for resale.

-

The cost to purchase raw materials or parts to make, assemble or package a product.

-

The cost of labor to make, assemble or package a product.

-

The cost of labor to ship a product to your warehouse.

COGS for ecommerce sellers might also include things like:

-

The cost of freight from your supplier to your 3PL warehouse.

-

Any cost of labor to inwards goods your product into your 3PL warehouse.

-

Any taxes that add to the cost of the product. That’s things like tariffs and duties, rather than sales tax which is a consumption tax or income tax which is a profit tax.

What’s not included in COGS

Costs incurred after your product is sold won’t be included in COGS.

And anything not directly related to producing or procuring your products isn’t part of COGS either.

Here are a few examples:

-

Labor and materials for picking, packing and shipping after your product has sold.

-

Salaries

-

Administrative and managerial costs

-

Rent

-

Marketing and advertising costs

-

Accounting and legal fees

The value of inventory youhaven’t sold isn’t part of COGS either.

Unless you use the cash accounting method, but we’ll get to that in a moment.

Are overheads included in COGS?

“Companies that really have this dialed in will take a percentage of overhead as COGS.”

- Lior Zehtser, Co-founder, ConnectCPA.

A percentage of overheads and utilities can be included in COGS if they’re directly related to producing your inventory. That’s things like machinery maintenance and warehousing.

This can be a bit of a gray area, so it’s always best to consult an expert like Connect CPA.

The three steps to calculating Cost of Goods Sold?

Let’s take another look at the formula for COGS:

Before you can use the formula you’ll want to pay attention to a couple of other things.

1. Know your inventory quantities

To figure out your COGS you’ll need some quantities.

For the time period you’re looking at:

-

How much inventory did you start with? This is called Beginning Inventory.

-

How much inventory have you purchased during this period? These are your purchases.

-

How much inventory have you ended up with? This is your Ending Inventory.

Your inventory management software should track this for you. But it’s important to verify the numbers on your books with a physical inventory count.

“Software is amazing, it runs the world… But it’s always good to complement your software with an actual inventory check or stocktake to double check that things match.”

- Lior Zehtser, Co-founder, ConnectCPA.

An inventory count means physically counting the inventory you have on hand. This includes inventory at all stages of production, including raw materials.

You should carry out these checks quarterly.

2. Know the value of your inventory

Once you have your quantities it’s time to work out how much each inventory item is worth.

There are four common methods for valuing inventory.

First in, first out (FIFO)

First in, first out assumes that the oldest item you purchased is the first one you sell.

FIFO is closest to the way most businesses sell their inventory.

Last in, first out (LIFO)

Last in, first out assumes that the newest item you purchased is what you sell first.

Some countries don’t allow the use of LIFO, so make sure to

consult an accounting professional before choosing this method.

Average Cost Method (ACM)

Average Cost Method takes the total cost of your inventory and divides it by the amount of items purchased.

Then this average cost is applied to all your inventory.

ACM is less precise than other methods, but it’s simple and reliable to work out. This makes it well suited for smaller businesses.

Specific Identification

The Specific Identification method values each item uniquely.

This method is very accurate, but it’s labor-intensive. It’s best suited to sellers who produce a small number of unique or high-cost items.

3. Use the formula for COGS (with example)

Now we have the data we need, let’s try an example.

Candy’s Cupcakes:

-

Valuation: Candy has used Weighted Average Cost value their inventory at $4.50 per cupcake.

-

Beginning Inventory: Candy’s Cupcakes started the quarter with 200 cupcakes.

200 x $4.50 = $900

- Purchases: During the quarter, they produced 400 more cupcakes.

400 x $4.50 = $1,800

- Ending Inventory: Candy 100 cupcakes left at the end of the quarter.

100 x $4.50 = $450

Let’s apply the formula:

$900 (Beginning Inventory) + $1,800 (Purchases) - $450 (Ending Inventory) = $2,250.

Candy’s Cupcakes COGS for the last quarter is $2,250.

Cash vs accrual accounting and COGS

Your accounting method affects how and where COGS shows up on your financial statements.

Let’s take a closer look.

Cash accounting might skew your data

In cash accounting, inventory never crosses your balance sheet.

You don’t recognize it as an asset.

Instead, inventory goes straight onto your income statement as an expense when you buy it.

Let’s say you buy 400 cupcakes for $1,800 in May. From May to August, you sell 100 cupcakes per month.

With cash accounting, your income statement will show $100 in sales and $1,800 in COGS for May. For June, July and August your sales will still be $100, but your COGS will be $0.

It seems like you’ve had a horrible month followed by several amazing months. There’s no relationship between your COGS and your revenue.

“If you don’t have COGS recorded in relation to revenue, you’ll have no idea whether your business is actually going to make money and be sustainable.”

- Lior Zehtser, Co-founder, Connect CPA.

Accrual accounting is the right fit

Accrual accounting creates a relationship between COGS and revenue.

Inventory is recorded as an asset on your balance sheet when you get it. As inventory is sold, the value of that inventory enters your balance sheet as a COGS expense.

This spreads your COGS evenly across the year. And COGS makes up a similar percentage of your sales each month.

You’ll have a more accurate view over how your business is actually performing.

Common COGS mistakes

Keeping accurate COGS is important, but it isn’t always easy.

Here are a few common errors to watch out for.

Using cash accounting

Cash accounting records your product purchases as COGS as soon as you buy them. This results in skewed and disjointed books.

Top tip: Use accrual accounting. Our bookkeeping checklist shows you how to record your purchases correctly for the accrual method.

Recording the wrong things as COGS

Knowing what to record as COGS can be complex, especially when it comes to overheads.

Top tip: Consult a professional ecommerce accounting practice like Connect CPA

Overstating (or understating) your inventory

Overstating your inventory means recording more inventory than you really have.

Your COGS will appear lower, and your profits higher. When it comes to tax time, you’ll end up paying more than you should.

Top tip: Double check your inventory numbers with regular physical inventory counts

Use the right tools for the job: Download our free checklist

There’s more to Cost of Goods Sold than meets the eye.

But the right tools can make it simpler. Apps like Dear Inventory, Cin7 and A2X can help you manage your inventory and calculate COGS accurately.

You can also download our Essential Ecommerce Bookkeeping Checklist. This free resource is the easiest way to make sure you’re doing your ecommerce bookkeeping right.

It walks you through all the best-practice processes for inventory and other bookkeeping tasks.

Download the Essential Ecommerce Bookkeeping Checklist and win at bookkeeping.

Want to feel completely confident in your ecommerce bookkeeping?

Businesses that document their processes grow faster and make more profit. Download our free checklist to get all of the essential ecommerce bookkeeping processes you need every week, month, quarter, and year.

Download it here